Why entrepreneurs should have a property investment business, and why they should structure it in this way.

Nathan is an entrepreneur and private equity investor of over 12 years. He’s started, grown and sold companies in the medical sector. With a passion for property, he owns a portfolio across the UK, but is now an FCA registered private lender and investor, with investments in over 14 businesses.

In this article, I thought it would be good to go over some of the actions that I think entrepreneurs and business owners should be undertaking in order to safeguard their future as well as how to grow and stabilise their income, especially for those businesses that are subject to seasonality.

We all know that property is a good place to store capital, and many business owners are already aware of this. But it’s also a great way to build up a secondary income stream that complements the income received from your primary business. It also helps to “flatten” out seasonal or volatile demand. In addition, whilst your business will help build your investment portfolio, as time goes by, the portfolio will then help grow your business, and so on. Having property and investment equity to leverage against can help give your business access to a greater scope of capital for re-investment and, subsequently, greater profits.

When I mention this, many entrepreneurs’ eyes glaze over – property can seem a boring and slow concept to a fast-moving business owner. But it needn’t be. Since building my own portfolio, the correlation between the success of my property and business is very much apparent – they feed off one another. And property can be fun!

One way to achieve this is to move profits from your trading business to your property investment business. This needn’t trigger taxable events either; you can use mechanisms like inter-company loans, or dividends if your investment business owns your trading business. Corporate dividends – ie: one company paying another company a dividend – are tax free almost all of the time (always check this with your chartered accountant or tax adviser, though).

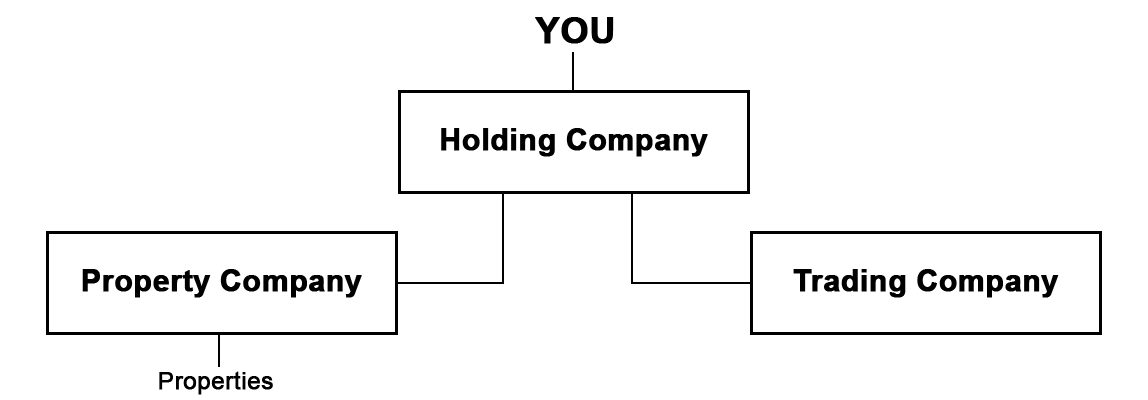

Once this money is available to your property business, you can start having fun. One important point to stress is that this activity should be kept separate from your trading business so that you don’t mix liabilities and associated risks. To do this, many of us use the following structure:

In a simple company group structure like this, a business owner is able to move money around efficiently, while at the same time protecting assets from the risks of day-to-day operations and trade creditors. For example, you don’t want a rowdy cardboard supplier chasing payments from a business that owns all of your property…

As your trading business feeds capital into your property business, which in turn invests this money and grows, your equity in those investments will also grow. This means that in future you can leverage commercial loans against that equity which can then go back into your business to help it expand, and vice versa, supercharging your growth.

The holding company

So what is a holding company? Simple, a holding company is a company set up to own the shares in another company. It doesn’t usually produce any products or services itself, and does not trade. However, what it does do is allow you to do a variety of beneficial things to help you be as tax efficient as possible, especially if your plan is to invest the majority of the earnings from your businesses. Some of these benefits can include:

For a holdings company that provides no products or services, tax at this level can be as low as zero. Dividends paid to your holding company from your other companies aren’t taxed and there is no capital gains tax on the disposal of company shares (where the holding company owns more than 30% of the share capital of the business and the whole shareholding is disposed – see ‘Significant Shareholder Exemption’). This could be a good way to sell your business, or your property portfolio as a whole – especially as Stamp Duty on company shares is much lower than it would normally be on property transactions. This gives you much greater flexibility.

It’s worth noting that many property lenders don’t like holding company structures. Owing to the ease at which you can move money around, lenders could see this as a way to ‘drain’ capital from your property company meaning that ostensibly the property company couldn’t meet its mortgage obligations. Now, obviously you wouldn’t do this, but it’s a risk to the lender. However, in many situations, you’ll be looking to filter profits from your business, so assuming purchases are in cash (which is how we do it in our business) then this won’t be an issue. And, having said this, it isn’t a problem for all lenders. Another alternative is to become a lender, which is what we did – thus earning a commercial rate on the money you filter into your investment company.

Hopefully this has given you an introduction to having a property investment business and a holding company structure. Next time we will look at special-purpose vehicles to make short-term property investments such as flips.

Disclaimer

This article was written in August 2020. I am not an accountant or tax professional. You should always discuss your personal circumstances with an accredited tax professional as tax legislation is subject to change.